How to Actually Get an EV Loan Approved on the First Try

Lakshay Khanna·15 June 2026

A friend called me in March, properly annoyed. He'd just been rejected for an EV loan on a Tata Tiago and couldn't understand why. Good salary, software job, no defaults that he knew of.

I asked him to send me his bank statement screenshot. He did. First thing I saw: salary credited on the 1st, and by the 27th of every single month the balance was under 800 rupees. Every month. Clockwork.

"Bhai tu kamaata theek hai par bachaata kuch nahi. Lender ko lagta hai tu already edge pe hai."

He went quiet. Then, "Yeh toh kisi ne bataya hi nahi."

Nobody tells you. That's the whole problem with loan approvals in India. Everyone tells you to "maintain a good CIBIL" and stops there, like that's the only lever. It isn't. I've watched people with 780 scores get rejected and people with 710 sail through, and the difference was almost never the score itself. Often it's pure admin — the kind our loan rejection reasons guide breaks down, from a PAN-Aadhaar name mismatch to a dead mobile number.

So this is the actual checklist. The stuff that decides whether your EV loan gets approved the first time, instead of you collecting rejections and tanking your own CIBIL in the process. (Already been rejected? Our EV loan rejected guide covers the 7 reasons and how to recover.)

Want a straight answer before you risk an inquiry?

Credifin reads your real income and tells you what to fix before it costs you a hard CIBIL pull. Decision in 3-7 working days, online.

Check My Eligibility →First, know which door you're knocking on

Most first-try rejections happen because people walk into the wrong lender for their profile. Not because they're un-loanable.

Salaried with a clean salary account goes to a bank. You'll get the best rate there, 12 to 14 percent, no reason to pay more.

Self-employed with conservative ITR, or a gig rider, or anyone whose income doesn't show up as a tidy monthly salary credit, goes to an NBFC. Banks will reject you not because you're risky but because their system has no box to put you in. NBFCs read bank statements and platform payouts. The rate's a bit higher, 14 to 19 percent, but it's an approval instead of a no.

Walking into the wrong one is how a perfectly fundable person ends up "rejected." It was never about you. It was the desk you sat at. Our bank vs NBFC guide has the full breakdown of which door fits which profile — read it before you pick.

The bank statement matters more than your score

This is the part nobody talks about. Lenders pull your bank statement and they read it like a story. Not just "how much comes in" but "how does this person handle money." It often matters more than the raw CIBIL score itself.

Things that quietly kill applications:

| What lenders see on your statement | What it reads as | Fix before you apply |

|---|---|---|

| Balance hitting near-zero every month-end | Already stretched | Keep a buffer for 3-6 months |

| A bounced auto-debit or cheque (even one) in 6 months | Instability | Zero bounces for 6 months |

| Regular transfers to Dream11, MPL, Rummy Circle | Gambling-app outflows — high risk | Stop 3-6 months before applying |

| Sudden lump-sum padded in 2 days before applying | Faked balance (now pattern-detected) | Build a genuine balance over months |

So before you apply, spend three to six months making your statement look boring. Keep a buffer. Don't let anything bounce. Boring is exactly what a lender wants to see.

One thing people try that doesn't work anymore: dumping a lump sum in two days before applying to fake a healthy balance. Banks have pattern detection now. A sudden pad right before an application looks worse than a low balance, honestly.

Don't apply at five places "to see who says yes"

I cannot say this loudly enough. Every application is a hard CIBIL inquiry. Each one knocks 5 to 10 points off. Stack four or five in a couple of weeks and you've personally engineered the rejection you were scared of.

Pick one bank and one NBFC. Apply at both, parallel, same week. That's it. Two inquiries is fine. Five is self-sabotage.

If both say no, stop. Wait 60 to 90 days. Inquiries fade, the score recovers, and you fix whatever the real issue was in the meantime. Then try again, once. If a string of rejections is the only problem, our guide on bouncing back from loan rejection walks through the recovery path.

Get your EMI-to-income honest before you walk in

Quick rule lenders use: all your EMIs put together, including the new one, shouldn't cross about 50 to 55 percent of your take-home.

Take-home 60,000, you're already paying 18,000 in EMIs, your new EV EMI ceiling is roughly 15,000. Push past it and you'll get rejected even with a great score.

If you're over the line, three options. Foreclose a small existing loan. Clear the credit card you've been revolving. Or add a co-borrower, spouse or parent with decent income, and the combined number works. The co-borrower route is the most underused fix I know of.

Sort the boring documents nobody checks until it's too late

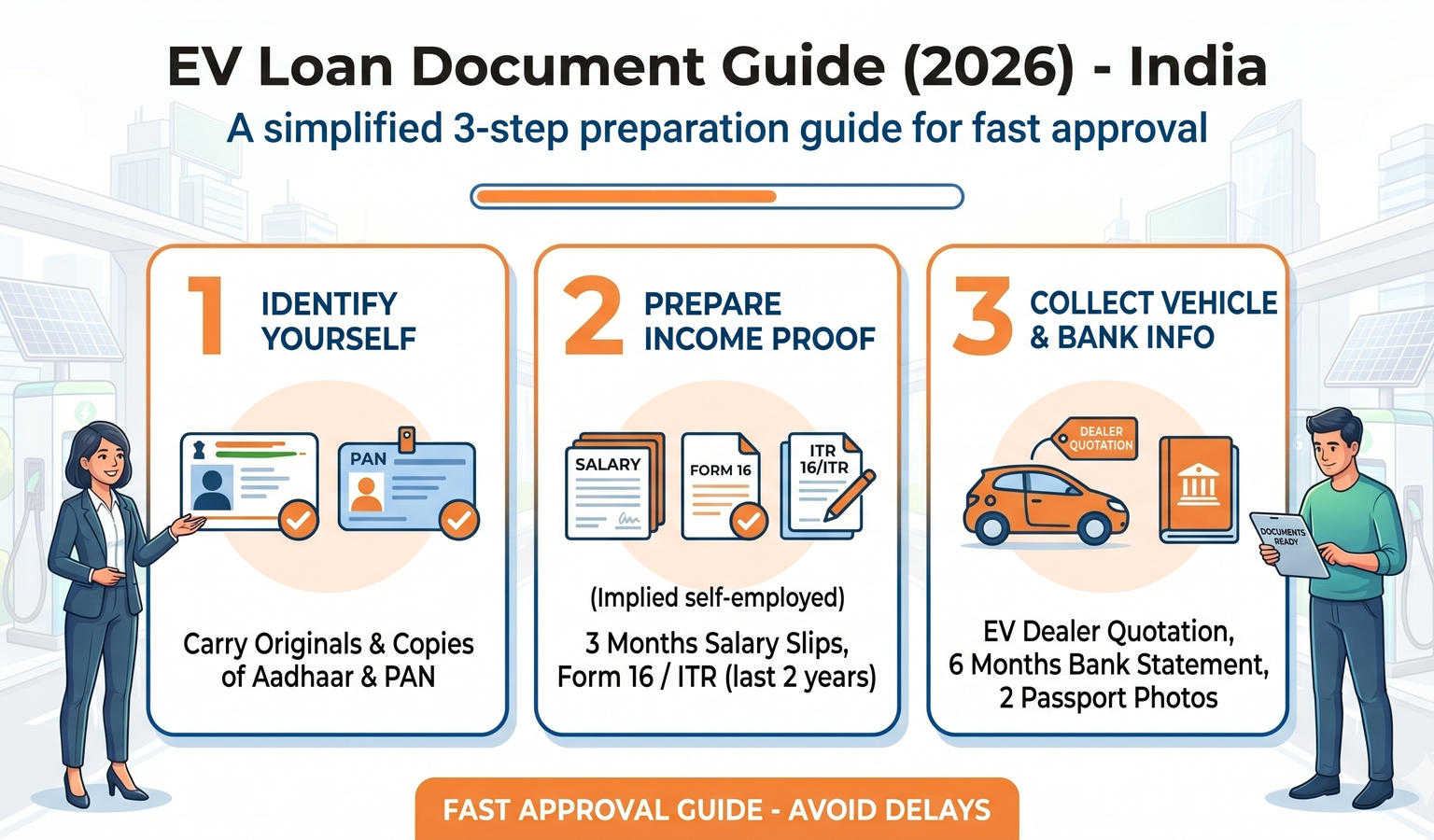

Most first-try rejections aren't dramatic. They're paperwork. The full list is in our EV loan documents checklist, but the three that sink the most applications:

Aadhaar address not matching where you live now. You moved cities for work, Aadhaar still shows the old town. Lender wants address proof to match. Update it first, costs almost nothing, takes about 10 days.

Job under six months at the current employer. Banks want tenure. If you just switched jobs, either wait it out or go NBFC, which is more relaxed if your previous job had a long run.

Gig riders, keep the platform partner ID screenshot and the bank account where payouts land. That account is your salary slip. Highlight the Zomato or Swiggy credit lines on the printout before handing it over. Executives scan, they don't read. Saves you a day. There's a dedicated walk-through in our EV loan for delivery riders guide.

A quick rate reality check

So you know what "approved" should actually cost you:

| Profile | Typical Rate | Tenure |

|---|---|---|

| Salaried, CIBIL 750+ | 12% to 14% | Up to 7 yrs (car) |

| Salaried, CIBIL 700-750 | 13% to 15% | Up to 4 yrs |

| Self-employed, clean ITR | 13.5% to 16% | Up to 5 yrs |

| Gig / cash income | 15% to 19% | 2 to 3 yrs |

The working band is 12 to 19 percent. Anybody quoting you above 19 for a normal profile is overcharging, and there's a cheaper lender out there you just haven't met yet. Walk.

Back to my friend

He didn't do anything dramatic. Stopped applying, first of all. He'd already hit three banks by the time he called me, which explained part of it.

Then he just kept a buffer in his account. Didn't let it crater at month end. Set the salary to auto-sweep a few thousand into a separate account he didn't touch. Three months of that and the statement told a completely different story.

Applied again. One bank, one NBFC. The bank approved at 13.5 percent.

He texted me after. "Yaar maine kuch bada nahi kiya, bas account theek dikhne laga." Exactly. He didn't become a better borrower. He just stopped looking like a worse one.

That's most of approvals, honestly. You're rarely as un-fundable as the rejection makes you feel. Usually one fixable thing is dragging the whole file down.

Make your file look its best, then apply once.

Tell us your profile and we'll flag anything that needs fixing before it costs you an inquiry — then approve on your real income. Decision in 3-7 days.

Apply for an EV Loan →Where Credifin fits

We're an NBFC, so the people who come to us are often the ones banks couldn't slot, self-employed with messy ITR, gig riders, cash-income traders, or folks who got rejected once and panicked.

We read the bank statement and the actual income, not just the tax filing. If the money's moving and the profile holds up, we approve on that. Rates land 13 to 17 percent depending on profile. Online application, decision in 3 to 7 working days. Credifin is an RBI-registered NBFC.

And if you've been rejected purely from inquiry stacking, tell us. That's underwritable. A pile of recent rejections isn't the same as being a bad borrower, and we can usually see the difference.

Bottom line

Getting an EV loan approved on the first try isn't luck. Walk into the right lender for your profile. Make your bank statement boring for a few months first. Keep your EMI-to-income under control. Sort the Aadhaar and tenure stuff before applying — update Aadhaar at any UIDAI centre if you've moved. And do not, ever, shotgun five applications hoping one sticks.

Do those, and the first try is usually the only try you need. And while you're at it, dodge the other money traps in our 9 first-time EV buyer mistakes guide.

FAQs

Why do people with good CIBIL still get rejected?

Usually the bank statement, EMI-to-income ratio, address mismatch, or short job tenure. The score is just one input.

How many lenders should I apply to?

One bank, one NBFC, parallel. No more. Each application is a hard inquiry that costs you points.

How long before I reapply after a rejection?

60 to 90 days. Inquiries fade, your score recovers, and you fix the real issue in between.

Does a co-borrower help?

A lot. Adding a spouse or parent with decent income and CIBIL often gets you approved and at a better rate.

Bank or NBFC for first-try approval?

Salaried with clean income, bank. Self-employed, gig, or cash income, NBFC. Matching this right is half the battle.

Will checking my own CIBIL hurt it?

No. That's a soft inquiry. Only lender pulls (hard inquiries) affect the score.

What rate should I expect today?

12 to 19 percent depending on profile. Above 19 for a normal profile means you should shop elsewhere.

Fastest way to approval?

Right lender, clean 6-month bank statement, documents ready, EMI-to-income under 50 percent. NBFCs can disburse in 3 to 7 days.

Ready to apply?

Want your EV loan approved the first time? Apply with Credifin online. We read your real income, not just the tax return, and tell you straight if something needs fixing before it costs you an inquiry. Decision in 3 to 7 days, pan-India.

Apply for an EV LoanThis might catch your interest