EV Loan for Delivery Riders: How Zomato & Swiggy Riders Get Approved When Banks Say No

Lakshay Khanna·10 June 2026

I was getting a food delivery last week and got talking to the rider while he waited for the lift. Swiggy guy, mid-twenties, riding a beaten-up petrol Activa. I asked, half making conversation, why he hadn't switched to electric yet given how many of his colleagues had.

"Sir loan nahi milta humein. Bank wale bolte hain salary slip dikhao. Ab main kahan se laaun salary slip?"

That line stuck with me. Because he genuinely wanted the EV, the math obviously worked for him, and the only thing standing between him and it was that a bank wanted a document his job will never produce.

He's not alone. There are lakhs of delivery riders in exactly this spot. Earning steadily, burning a fortune on petrol, and locked out of the one thing that would fix it, because the banking system doesn't know how to read their income. So this is for every Zomato, Swiggy, Blinkit, Zepto, and Uber rider who's been told no. Here's how you actually get approved.

Ride for Zomato, Swiggy, Blinkit, Zepto, Uber, or Rapido?

Skip the bank that already said no. Apply with Credifin online, we read your platform payouts as income. No salary slip needed. Decision in 3-7 days.

Apply for Rider EV Loan →Why banks keep saying no (it's not about you)

Let me kill the shame around this first, because riders carry it and they shouldn't.

The bank's tool is the limit, not your income.

A bank's loan system is built to read one thing well: a salary slip plus a salary credit landing on the same date every month. That's its comfort zone. Feed it that, it's happy. Your payout-based income doesn't fit that template, so the system defaults to no. Not because you don't earn — you might out-earn the salaried guy it just approved — but because it can't read how you earn.

So when the bank says no, it isn't a judgment on your finances. It's an admission that their tool can't process your kind of income. Different problem entirely.

Who reads a rider's income properly: NBFCs

NBFCs were basically built for the income types banks can't handle. A good NBFC doesn't ask a rider for a salary slip. It asks for two things, your platform partner ID and the bank account where your payouts land, and then it reads the actual money.

It looks at your statement and sees, say, 25 to 35 thousand landing every month from Swiggy or Zomato, consistently, for the last year. To an NBFC, that pattern is your salary slip. Steady platform payouts are proof of income, and a rider with a year of them is a perfectly fundable borrower.

That's the whole unlock. You don't need to become a different kind of worker. You just need a lender that reads payouts instead of demanding slips. The broader picture is in our EV loan India guide if you want to see how all profiles compare. Riding in Noida or Greater Noida? Our EV loan in Noida guide covers local dealers, e-rickshaw finance, and real EMI numbers for the sectors.

Bank vs NBFC for a delivery rider

| Lender's question | Bank | NBFC (Credifin) |

|---|---|---|

| Salary slip? | Required | Not needed |

| Employer letter? | Required | Not needed |

| Platform partner ID? | Ignored | Primary proof of work |

| Payout bank statement? | Ignored | Primary income proof |

| 6-month statement required? | Sometimes | Always — critical |

| Guarantor needed? | If credit thin | Only for new platforms (under 6 months) |

| Likely outcome for a rider | Rejection | Approval |

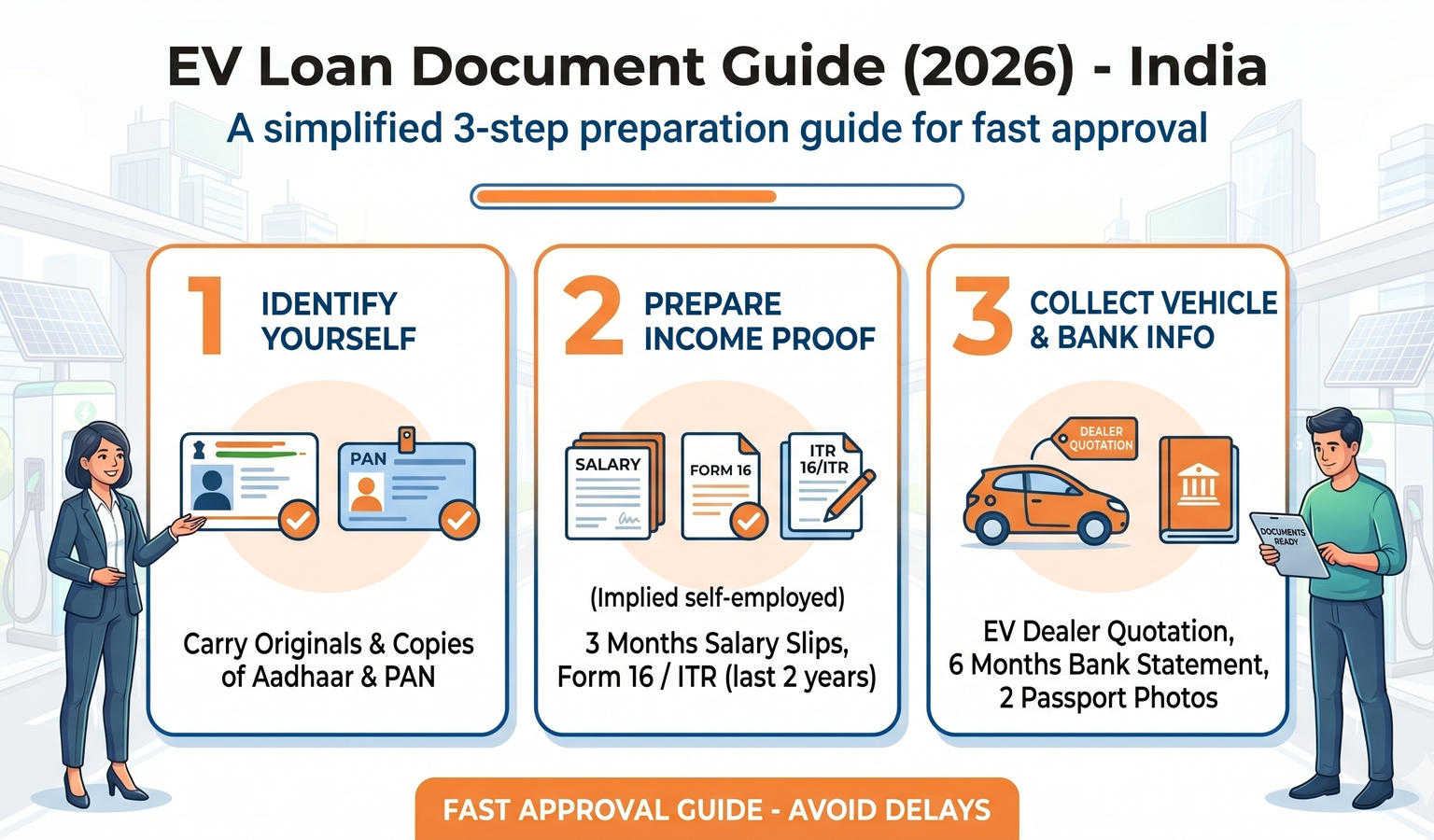

What you actually need to get approved

The list is short, and none of it is a salary slip:

Screenshot from the Zomato, Swiggy, Blinkit, Zepto, Uber, or Rapido app.

Of the account where your payouts land. Your income proof.

Update your Aadhaar at UIDAI first if you've moved cities.

Mainly if you've been on the platform under six months.

That's genuinely it. If you've been riding steadily for a year and your payouts land in one account, you're most of the way there already. The full checklist by profile is in our EV loan documents checklist.

💡 The one trick that speeds it up

Small thing, real difference. When you hand over your bank statement, the payout lines are scattered among all your other transactions, recharges, UPI to friends, the lot. The loan executive scans fast and might not register how steady your income actually is.

So before you submit it, highlight every payout line, the ones that say "Swiggy" or "Zomato" or the platform's UPI handle. Make your income jump off the page. It sounds trivial but it genuinely helps the person assessing you see the pattern instantly, and that can shave a day off your approval.

The math that makes this worth it

Here's why riders want this so badly, and why it works.

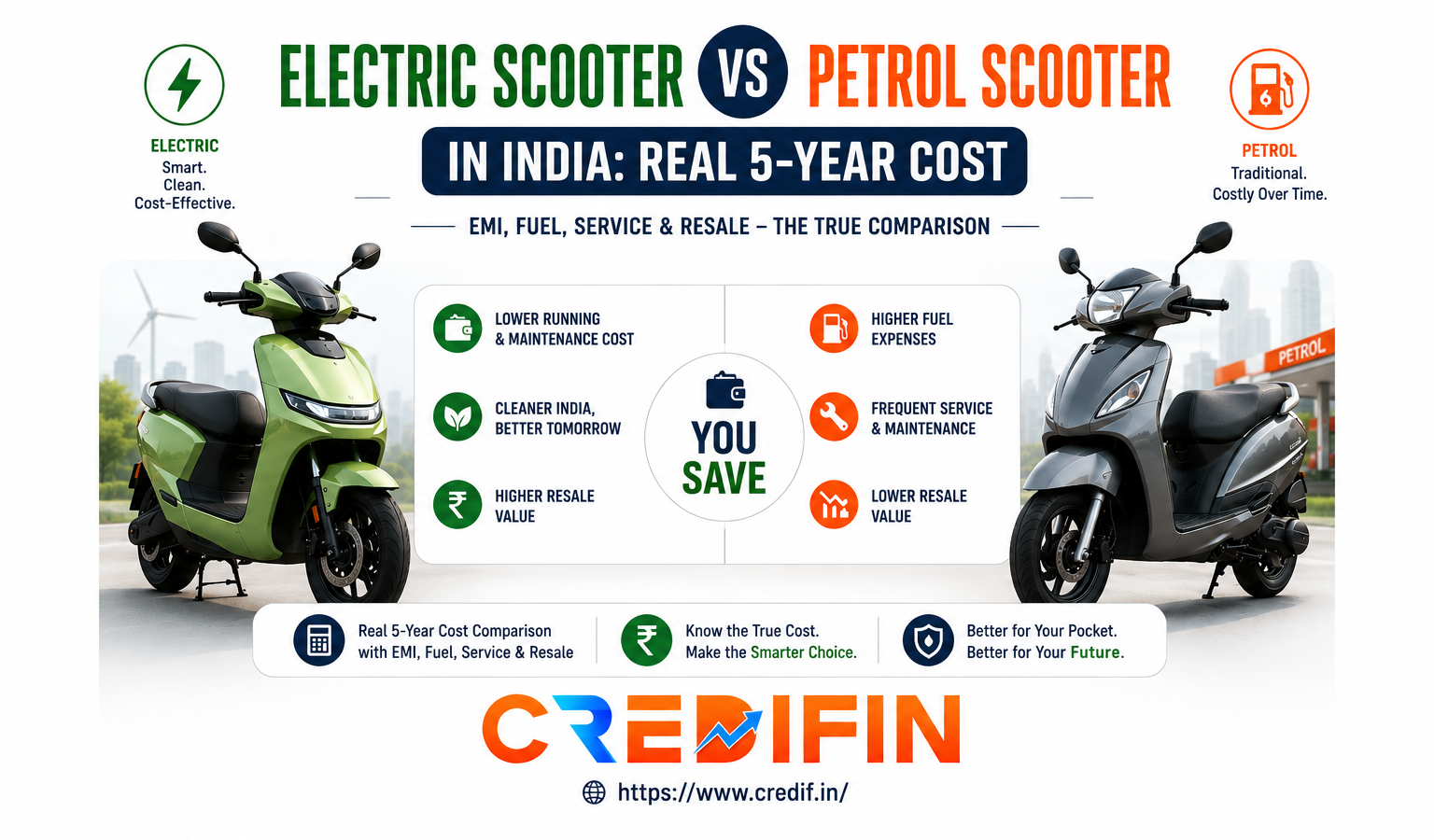

A delivery rider on petrol, doing those short stop-start runs all day, the worst case for mileage, often burns 200 to 300 rupees a day in fuel. Call it 6,000 to 8,000 a month, gone.

The same daily distance on an EV scooter costs 30 to 50 rupees in electricity. Maybe 1,200 to 1,500 a month. So you're saving in the region of 5,000 to 6,500 every month just on fuel. The fuller cost comparison is in our electric vs petrol scooter cost breakdown.

Now put that against the loan. An EV scooter financed over 30 months usually runs an EMI of around 3,500 to 5,500. Look at those two numbers side by side. Your fuel saving alone often covers the entire EMI, sometimes with money left over. The scooter pays for itself while you ride it, and at the end you own it outright. That's the rare loan that genuinely improves your cash flow from month one.

| Cost item | Petrol scooter | EV scooter on loan |

|---|---|---|

| Daily fuel / charging | Rs 200 to 300 | Rs 30 to 50 |

| Monthly fuel / charging | Rs 6,000 to 8,000 | Rs 1,200 to 1,500 |

| EMI (30 months, post-PM e-DRIVE subsidy) | — | Rs 3,500 to 5,500 |

| Total monthly outgo | Rs 6,000 to 8,000 | Rs 4,700 to 7,000 |

| You save every month | — | Rs 1,000 to 3,300 |

| After EMI ends | Petrol bill continues forever | EV owned, only Rs 1,200 to 1,500/mo charging |

Your fuel saving will cover the EMI from month one.

This is the rare loan that puts money back in your pocket immediately. Apply with Credifin in under 10 minutes, all online.

Apply Now →Back to the Swiggy rider

I told him most of the above, standing there by the lift. Told him to stop walking into banks, go to an NBFC, bring his partner ID and six months of his payout account statement, and update his Aadhaar if it still showed his hometown.

He messaged me a few weeks later, through the same delivery app actually. He'd got approved. Ola S1 X, financed, riding electric now.

"Sir ab petrol ka kharcha khatam, aur gaadi bhi apni. Bank ne mana kiya tha, par ho gaya."

Bank said no, and it still happened. Because the no was never about whether he could afford it. It was about whether anyone would read his income properly. Someone finally did.

A note on rates

Rider and gig profiles usually land in the 14 to 18 percent range, the higher end of the overall 12 to 19 percent vehicle loan band, because there's no salary slip and the income reads as less "stable" on paper even when it isn't. That's the honest trade. A slightly higher rate, but an approval and a vehicle that pays its own EMI, versus a cheaper rate at a bank you'll never actually qualify for. For most riders, that's an easy call. If you ever build a credit history and want to refinance, our CIBIL improvement guide walks through how.

Where Credifin fits

This is exactly who we built our underwriting for. We finance EV scooters for delivery riders across India, online, and we assess you on your platform payouts and bank statement, not a salary slip you'll never have.

Ride for Zomato, Swiggy, Blinkit, Zepto, Uber, or Rapido, bring your partner ID and six months of your payout account, and we read the actual income. First-timers under six months on a platform, we'll often work with a guarantor. Rates for rider profiles land around 14 to 18 percent, decision in 3 to 7 working days, and because the EV starts saving you fuel money immediately, the EMI tends to look after itself. If you'd rather start with a smaller down payment, the maths is in our EV down payment guide.

Bottom line

If a bank rejected you for a delivery-rider EV loan, the problem was never your income. It was that a bank can't read payout-based earnings. NBFCs can, and do, every day.

Bring your platform partner ID and six months of the bank statement where your payouts land. Get your Aadhaar address current. Go to an NBFC, not a bank. And remember the fuel savings usually cover the EMI on their own, so this is one of the few loans that puts money back in your pocket from the first month. The no you got was the wrong door, not the end of the road.

FAQs

Can I get an EV loan as a Zomato or Swiggy rider without a salary slip?

Yes, through an NBFC. They use your platform partner ID and bank statement showing payouts as income proof. Banks usually can't.

Why do banks reject delivery riders?

Their systems are built to read salary slips and fixed monthly credits. Payout-based income doesn't fit that template, so they default to no, even if you earn well.

What documents do I need?

Platform partner ID screenshot, six months bank statement of your payout account, PAN, Aadhaar with current address. Sometimes a guarantor if you're new to the platform.

How much can I borrow?

Enough for most EV scooters, typically 85,000 to 1.1 lakh after subsidies. The exact amount depends on your payout history and profile.

Will the EMI be affordable on rider income?

Usually very. EMIs run around 3,500 to 5,500 a month, and your fuel savings of 5,000 to 6,500 a month often cover that entirely.

Do I need a guarantor?

Mainly if you've been on the platform under six months with limited payout history. Established riders with a year of payouts often don't.

What interest rate will I get?

Generally 14 to 18 percent for rider profiles, the higher end of the 12 to 19 percent vehicle loan band, because there's no salary slip.

How fast is approval?

At an NBFC, usually 3 to 7 working days once your documents are in. The application is typically online.

Ready to apply?

Ride for a delivery platform and been told no by a bank? Apply with Credifin online. We read your platform payouts and bank statement as real income, no salary slip needed, and the fuel savings usually cover your EMI from month one. Decision in 3 to 7 days, pan-India.

Apply for an EV LoanThis might catch your interest