Electric Scooter vs Petrol Scooter in India: Real 5-Year Cost (EMI, Fuel, Resale)

Lakshay Khanna·26 May 2026

Ok so one of my friends from college, Rohit — works in some small CA firm in Phase 8 Mohali, nothing fancy — calls me up sometime in December last year. Properly frustrated. His Activa, which by the way isn't even his, it's his chacha's hand-me-down from like 2020 or 2021 I think, was eating him alive on petrol. Twenty-two km one way to office. Twenty-two km back. By November the monthly petrol spend was around Rs 2,800 and Rohit was doing that mental calculation we all do where you stare at the bill and feel slightly sick.

Anyway. He spent two weekends on it. Three dealer quotations, Excel sheet, the whole thing. January he bought an iQube. NBFC loan, 36 months. Now we're in May. His monthly electricity for the scooter is around Rs 290.

Big deal right, savings on petrol, everyone knows electric is cheaper to run. Sure. But the part that actually got him was this. His new monthly outflow on the iQube — EMI plus electricity — works out to roughly Rs 3,585. Earlier setup, paying his chacha back informally plus petrol, was around Rs 4,200. So he's saving 600 bucks a month with the more expensive scooter on EMI. Not later. Right now. From month one.

He didn't expect that. Most people don't.

Which is why I'm writing this. Because the calculation that decides electric vs petrol is not the one most buyers actually do at the dealer counter. They look at sticker price, get scared, and walk back to the Activa showroom. Fine. Sometimes that's the right answer. Sometimes it really isn't.

What petrol costs you right now

Activa 6G. Jupiter 125. Access 125. Between them, basically the entire petrol scooter market in Punjab right now. Maybe a bit of Pleasure Plus or Aviator on the edges. On-road in Jalandhar these days you'll pay between Rs 80,000 for a base Activa and around Rs 1.10 lakh for a top trim Access. Slight variation by RTO. Dealer offers come and go.

The prices haven't really moved. Two years. Honda did a small refresh on the Activa, TVS pushed Jupiter into 125cc territory, nobody really cared. Manufacturers know the buyer for these scooters isn't price-sensitive to the rupee — they want reliability, mileage, service network. Honda has all three. Job done.

What did move was the fuel. Petrol in Punjab right now, I checked yesterday, is sitting at 96 rupees and some change. A year back it was 94. Two years it was 91. Doesn't sound dramatic. But when you ride 1000 km a month for five years, that 5 rupee difference per litre matters. It just keeps quietly compounding.

What electric costs you right now

The market has split into three layers now and you should know what you're shopping.

Bottom end is the Ola S1 Z type stuff. Vida V2 base. Hero Vida entry. Anywhere from 60k to 80k ex-showroom. Small battery, basic features, 60-70 km real range on a good day. Fine for short commutes if your budget is tight. Don't expect frills.

The serious middle is where most buyers end up. iQube base, Chetak 2501 and 3001, Rizta. Ex-showroom 94k to 1.20 lakh. Real range somewhere between 80 km and 130 depending on the variant. This is what I'd actually recommend for a regular city rider.

Premium — Ather 450X, the top spec iQube ST, Ola S1 Pro — 1.40 lakh and going up to like 1.55-1.60 if you load it up. Worth it if you care about touchscreen dashboards and ride quality. Most people don't need this.

The PM E-DRIVE subsidy is still on. For now at least. Rs 2,500 per kWh of battery capacity but they've capped it at 5,000 rupees per vehicle, which honestly is a bit stingy when you compare to what FAME II was doing. Whatever, 5k is 5k. It comes off the dealer invoice automatically, you don't have to apply for anything. Delhi, Gujarat, Maharashtra throw in state subsidies on top. Punjab? Nothing meaningful right now. We get the central one and that's it.

End result: iQube base on-road in Jalandhar comes to about 1.15 lakh. Jupiter 125 on-road, comparable middle-segment petrol, is around 96k. Difference of nineteen thousand rupees.

That nineteen thousand is the whole thing. The whole debate boils down to whether the running cost savings cover that gap before the loan ends. Spoiler: yes, and easily.

EMI — and why banks and NBFCs are different planets

Quick refresher because people get this wrong.

Two-wheeler loans in India right now — banks are giving roughly 10.5 to 13 percent. But only to salaried people with CIBIL above 750 and clean documentation. Form 16, salary slips, six months of bank statements, the whole works. If you tick those boxes, walk into HDFC or ICICI and you'll get a good rate.

NBFCs are different. They run higher — usually 12 to 16. Sometimes touching 17 for first-time borrowers without any credit history. The reason isn't that NBFCs are greedy. It's that they're underwriting the people banks already rejected. Self-employed shopkeepers in Bus Stand area, gig workers, the guy doing deliveries for Borzo who can't show a salary slip, students whose parents are co-applicants, CIBIL 680 because of one bounced EMI in 2022. Banks say no in eight minutes. NBFC actually looks at the file. If your CIBIL is sitting in the 650-720 band, our CIBIL improvement playbook covers how to push it past the bank threshold over 8 to 12 months.

EV loans are about one percent more expensive than petrol at the same lender. Stated reason is "resale uncertainty." Real reason is EV is still a newer asset class. This gap will close. Right now you pay it.

Let me run a few EMIs assuming 85 percent loan, 36 months.

| Scooter | On-Road Price | Loan Amount (85%) | Interest Rate | Monthly EMI |

|---|---|---|---|---|

| Activa 6G (petrol) | Rs 88,000 | Rs 75,000 | 12% | Rs 2,485 |

| Jupiter 125 (petrol) | Rs 96,000 | Rs 81,600 | 12% | Rs 2,710 |

| iQube base (electric) | Rs 1,15,000 | Rs 97,750 | 13% | Rs 3,295 |

| Chetak 3001 (electric) | Rs 1,20,000 | Rs 1,02,000 | 13% | Rs 3,495 |

| Ather 450X (electric) | Rs 1,55,000 | Rs 1,31,750 | 13% | Rs 4,440 |

The bit that matters: iQube vs Jupiter, like-for-like middle of the market — Rs 585 difference per month. Electric is the higher one.

585 rupees. That's where most people stop reading the comparison and walk away thinking petrol is the cheaper option.

It isn't. Not even close. Let me show you why.

Where the actual money is hiding

I'm gonna use 1000 km per month for the math because that's roughly what an average Indian commuter does. Office in a metro 35-40 km a day, six days a week, plus weekend errands. Your number might be higher if you're in sales or delivery, lower if you live close to work. Doesn't matter, the math scales.

Activa real mileage — 45 to 50 kmpl in Indian city traffic, lower in summer with AC… wait scooters don't have AC, scratch that. Lower in summer though, more battery drain on… no, lower because of engine heat and more idling. Anyway. Call it 47.5 kmpl average. Petrol at 96 rupees. You're paying about 2 rupees per km in fuel. Round number, easy.

iQube — full charge takes about 1.5 units. That gives you 80 km of real range. Domestic electricity in Punjab is 7 per unit roughly (depends on slab but let's go with that). Works out to almost 13 paise per kilometre. Yes paise. Not rupees. I had to recheck this when I first did the math.

1000 km a month. Petrol bill: 2,000. Electricity: 130. Saving: 1,870 every single month.

Now put it next to the EMI. The petrol scooter's EMI was Rs 585 cheaper. So your real monthly position on the electric is 1870 minus 585 — about Rs 1,285 better off. With electric. Every month. Net of EMI. After everything.

Across one year that's 15,400 in your pocket. Across the three year loan tenure — 46k. And we haven't even talked about service yet.

The service bill nobody factors in upfront

Petrol scooter needs oil every 3000 km or thereabouts. Each change is about 400-500 by the time you add labour and the consumable bits. You'll do three or four a year easily if you ride properly. General service every six months, anywhere from 700 rupees to 1200 depending on what's needed. Then over three years you'll burn through an air filter, possibly a plug, definitely a drive belt. Another 2-3 thousand right there. Plus the random stuff. Clutch slipping. Bearing gone. Carb cleaning. Indian roads will find a way to make your scooter cost money.

There's an Activa guy who runs a kirana two buildings from mine. Asked him casually one evening — said he'd spent about 5,200 on the scooter in 18 months. Sounded about right to me.

Electric scooters are structurally different. There's no oil. No filter. No spark plug. No carburetor. Nothing combusts. The motor is a sealed unit, the controller is a sealed unit, the battery is a sealed unit. There's almost nothing to service in the conventional sense. Annual service at iQube or Chetak authorised centres is around 1,500 to 2,500 rupees and most of that is brake checks and software updates. Tyres and brake pads wear the same as petrol scooters so no advantage there. Battery is under warranty for 3 to 5 years from purchase, brand dependent. When the warranty ends, our EV battery replacement loan covers the swap so you don't pay 25-45k out of pocket.

Person I know in Mohali on an iQube — 1,800 spent in 14 months. Chetak owner near Bus Stand Jalandhar — 2,400 across 22 months and that included a new rear tyre. Not nothing. But miles away from what petrol burns.

Over five years the service gap alone is something like 15 to 20 thousand rupees, in favour of electric.

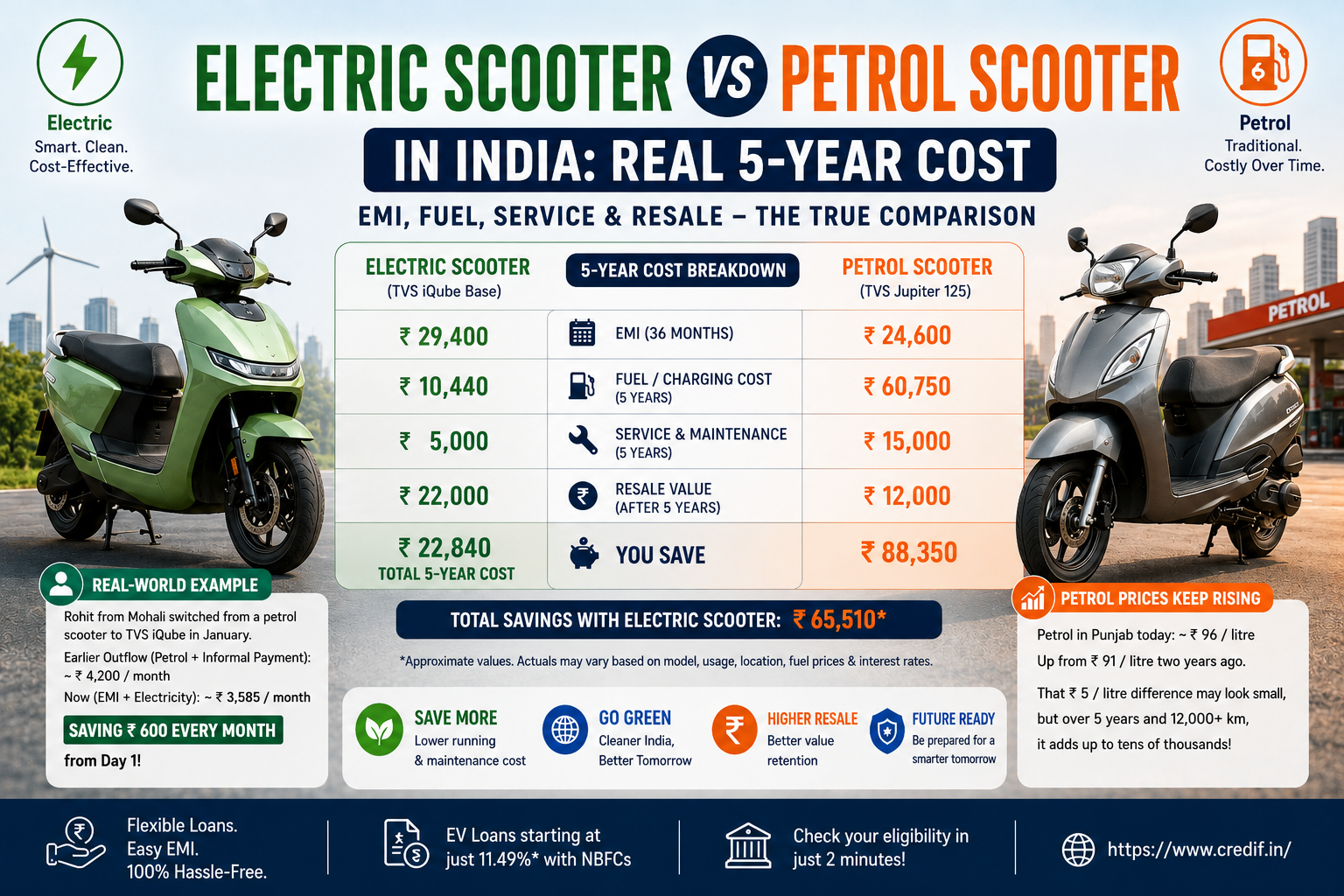

So what's the actual five-year cost

Let me do this for a middle-segment buyer, 36 month loan, planning to own the scooter for five years total, riding 1000 km a month.

| Cost Item | Jupiter 125 (Petrol) | iQube Base (Electric) |

|---|---|---|

| On-road price | Rs 96,000 | Rs 1,15,000 |

| Loan interest (3 years) | Rs 16,000 | Rs 20,800 |

| Fuel / electricity (5 years) | Rs 1,20,000 | Rs 9,000 |

| Service (5 years) | Rs 22,000 | Rs 8,500 |

| Insurance (5 years) | Rs 9,500 | Rs 11,000 |

| Resale at year 5 | - Rs 38,000 | - Rs 35,000 |

| Net 5-year cost | Rs 2,25,500 | Rs 1,29,300 |

Jupiter 125 buyer. Pays 96,000 on-road day one. Across the three year loan he pays about 16k in interest. Over five years of riding he burns about 1.2 lakh of petrol. That number alone should make anyone pause for a second. Then add 22k in service. About 9,500 in insurance. Resale value at year five is maybe 38k if the scooter is in decent shape. Net cost of owning the petrol scooter for five years works out to roughly Rs 2,25,500.

iQube base buyer. 1.15 lakh on-road. Loan interest over three years is about 20,800 because the loan is bigger and the rate is slightly higher. Five years of electricity — 9,000 total. Service across five years — 8,500. Insurance is a touch more expensive on EVs right now, partly because insurance companies are still working out how to price battery damage claims, so 11,000 over five years. Resale at year five — currently the secondhand EV market values a 5-year-old iQube around 35k. Net cost of ownership over five years — roughly Rs 1,29,300.

Difference is about 96 thousand rupees. Almost a full year of EMI saved over the five years. Just from doing the same thing electrically instead of with petrol.

Now I have to be honest about the wildcard which is battery. Most scooters have 3-5 year battery warranties. Out of warranty, replacement runs 25 to 45 thousand depending on model and battery chemistry. If you're planning to keep the scooter 8 to 10 years which a lot of Indians do, build that replacement into your math.

When you should just buy petrol and stop reading this

Honestly let me be straightforward here because I'm tired of EV evangelists pretending electric is right for everyone. It isn't.

Live in a rented flat where the society won't let you run a cable down to the parking area? Don't buy electric. Charging takes three to five hours. You need a plug point near where the scooter sits overnight. If that's not possible in your living arrangement, just get an Activa. Don't fight it.

Daily ride is longer than the scooter's real range and there's no fast charger anywhere convenient? You'll be doing range anxiety calculations every morning before leaving home. That mental load isn't worth the savings. Petrol.

Ride 5-8 km a day, total? Fuel savings will be too small to recover the upfront gap within the loan. Just buy petrol. Honda will keep selling Activas, they'll keep working for 12-15 years, you'll never think about your scooter again.

Most of your kms are highway at sustained 70-80? Electric scooters lose range fast at high speeds. Their published numbers are city numbers. You'll be disappointed. Get a petrol.

For everyone else though — anyone doing 25+ km a day mostly in city, with somewhere to plug in at night — electric is genuinely cheaper now. Two years back the math was iffy. It's not iffy anymore.

Suresh's story from Lamba Pind Road

There's a guy I know, Suresh, who runs a parts supply outfit somewhere near Lamba Pind Road in Jalandhar. His son was on an Activa doing deliveries to mechanics and workshops across the city. 60 km a day minimum, often 80.

Switched to a TVS iQube in March 2025. NBFC loan, three years, EMI 3,295. The Activa got sold for 32k to a tea stall guy nearby who needed a runaround.

Petrol on the Activa was running 3,400 monthly. iQube electricity is 380, slightly higher than a regular commuter would pay because deliveries are weighted — boxes of parts, motor pulls more, shows up on the bill. Net saving 3,020 a month.

What Suresh said when I last spoke to him — the EMI is basically being funded by the money they were spending on petrol anyway. After 12 months the cumulative savings have already paid for 11 months of the EMI itself. After three years the loan ends and they own the scooter free. His son keeps using it for deliveries.

He's not an EV person. Doesn't care about emissions. Switched because the petrol math had stopped making sense for the volume of riding his son does. That's it. If you're in Punjab and want a similar setup, our EV loan in Jalandhar guide walks through the local lender options.

How you should actually decide

Three things. Forget brand, forget colour, forget which influencer recommended what.

How far do you ride in a day. Under 15 — electric struggles to justify itself on math alone. 15 to 30 — works but payback is slower. Above 30 — clearly favours electric over 3 to 5 years.

Where will it park overnight. Got a plug point at home or shop where you can leave it charging from 10pm to 6am? Yes — electric is genuinely zero-hassle, you wake up to full battery every day. No — factor in the inconvenience of public charging, which is patchy at best in Punjab right now.

How long do you plan to keep it. Five years or more — electric wins on total cost handily. Two years — math is much tighter because petrol still has slightly better resale today.

Answer those three. That's your decision. Everything after is shopping for the variant and colour you like.

| Daily Riding | Payback Time | Verdict |

|---|---|---|

| Under 15 km | Beyond 3-year loan | Petrol — fuel savings too small to recover the gap |

| 15 to 30 km | 18 to 24 months | Borderline — electric works if you keep 5+ years |

| 30 to 50 km | 14 to 20 months | Electric — clear winner |

| 50+ km (delivery work) | 8 to 12 months | Electric — significant savings, fastest payback |

Frequently Asked Questions

Is electric scooter EMI really much higher than petrol?

Honest answer is yes, around 600 to a thousand rupees a month on a comparable middle segment loan. But the fuel savings every single month are usually two to three times that gap, so real net outflow is lower for almost any rider doing more than minimal commuting.

How long is the payback period?

30 km a day rider — upfront premium recovers in about 14 to 20 months. 50+ km a day, which is most delivery work — under 12 months, sometimes 8 months. Under 15 km a day — frankly, never within the three year loan, the math just doesn't work.

Does Section 80EEB tax deduction apply to electric scooter loans?

Section 80EEB under the Income Tax Act allows up to 1.5 lakh deduction on EV loan interest. The catch most articles miss: it only applies to loans sanctioned between April 2019 and March 2023. New loans taken today don't currently qualify. The government could reopen the window in a future budget. As of right now, no. Don't make a buying decision based on the assumption that this benefit will come back.

What is the battery replacement cost out of warranty?

25 to 45 thousand rupees depending on model and battery chemistry. Within warranty, manufacturing defects are free. Wear and degradation after the warranty period is your problem. See our EV battery replacement loan guide if you're planning ahead.

Can I ride an electric scooter in monsoon?

IP67-rated battery scooters handle normal rain. Don't ride either petrol or electric through knee-deep water. Common sense, but people forget when it's their daily route flooded.

Can I get an electric scooter loan with CIBIL below 700?

Banks will probably reject you. NBFCs like Credifin underwrite differently — they look at bank statement income and actual repayment capacity rather than just the credit score number. Approval at 650+ happens regularly when the rest of the file is okay. Our EV two-wheeler loan is built for this profile.

What's the used EV scooter resale market like?

Improving every year but still weaker than petrol. 5-year-old EV scooter today fetches around 30-35% of its original on-road price. 5-year-old petrol fetches 40-45%. Gap is narrowing as the used EV buyer pool expands.

Should I wait for next year's models?

Don't wait. The fuel savings you'd give up during that waiting year are usually larger than the price drop you're expecting on the next model. If you need a scooter now, get one now. Stop optimising for the perfect timing.

Ready to Apply?

Buying an electric or petrol two-wheeler? If you want a lender that actually evaluates self-employed people, gig workers, delivery riders, and folks whose paperwork isn't textbook — get a quote from Credifin online. We do both petrol and EV two-wheeler loans, same flexible underwriting.

This might catch your interest