EV Loan Documents Checklist: Exactly What to Carry to Avoid Delays

Lakshay Khanna·04 June 2026

A friend of mine went to a showroom three separate times for the same loan. Three trips. Because every time, the executive asked for one more document he didn't have on him.

First trip, missing the bank statement. Second trip, had the statement but it was only three months and they wanted six. Third trip, finally had everything, except the address proof had his old flat's address and his Aadhaar had the new one. Mismatch. Sent home again.

By the fourth visit he was ready to give up on the whole EV.

"Yaar har baar kuch na kuch reh jaata hai. Pehle hi list de dete toh ek baar mein ho jaata."

He's right. Nobody gives you the full list upfront. So here it is, profile by profile, the exact documents to carry so your EV loan goes through in one sitting instead of four. Get these ready before you walk in and you save yourself a week, easily.

Skip the four trips. Apply online in 10 minutes.

Upload your documents from home. Credifin flags anything missing upfront, in one go, not one at a time. Decision in 3-7 days.

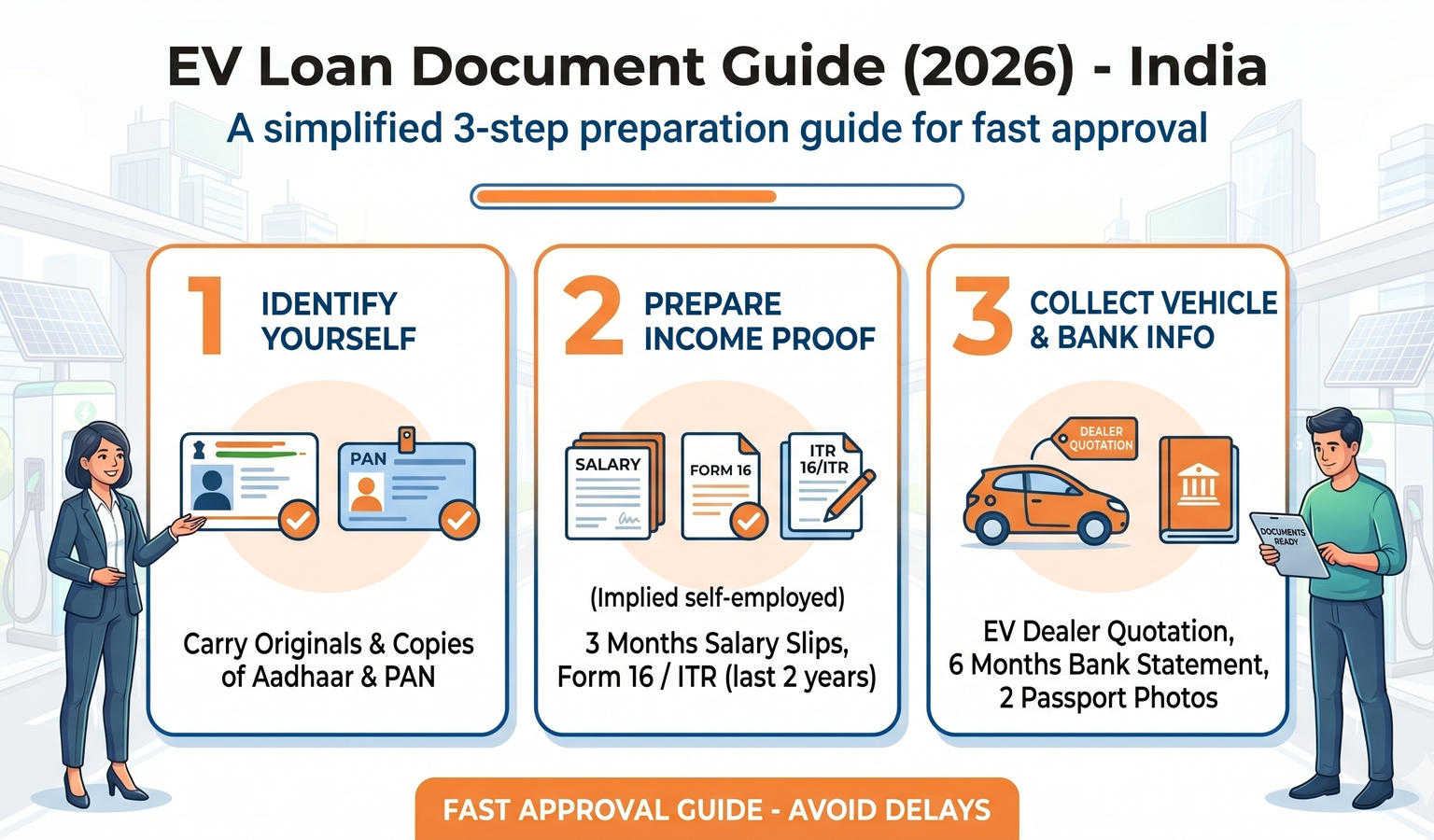

Apply Now →The documents everyone needs, no matter the profile

Some things every single applicant needs, salaried or not:

Non-negotiable. The whole credit system runs on it.

The address on it must match where you actually live now. (More on this trap below.)

Sounds trivial. People still show up without one and lose half a day.

Electricity bill, registered rent agreement, passport. Must be recent.

That's the base. Now the part that changes by who you are.

If you're salaried

The easiest profile, and the shortest list:

Three latest salary slips. Confirms your income, employer, designation.

Six months bank statement of your salary account. Not three. Six. This is the single most common reason salaried people get sent back. They bring three, the lender wants six.

Employer ID card or an offer/employment letter. Just to confirm you actually work where the slips say.

That's genuinely it for most salaried car or scooter loans. Have these four plus the base documents and you're usually approved in a single visit. Government employees in particular get the sharpest rates — see our government-employee EV loan guide.

If you're self-employed or run a business

More documents, because your income has to be reconstructed rather than just confirmed:

Two years of ITR with computation. Both, if you file personal and business separately.

Twelve months bank statement of your business account. They want to see turnover and consistency.

GST registration certificate, if your turnover crosses the threshold and you're registered on the GST portal.

Business proof. Shop license, Udyam registration, or a rental agreement for your business premises.

The thing self-employed people underestimate is how long it takes to dig out two years of ITR and a clean 12-month statement if you haven't kept them handy. Pull them before you start, not when the executive asks. We've covered the rate-side of this in detail in our self-employed EV loan guide.

If you're a gig worker (Zomato, Swiggy, Blinkit, Uber, Rapido)

Banks struggle with this profile, but the documents themselves are simple. The trick is knowing what stands in for a salary slip:

The partner ID screenshot from your platform app. This is your proof of work.

Six months bank statement of the account where your payouts land. This is your salary slip, effectively. The lender reads the payout pattern.

Address proof and the base documents.

Sometimes a guarantor, especially if you've been on the platform under six months.

💡 Pro tip: Before you hand over the bank statement printout, take a highlighter and mark every payout line — the ones that say "Zomato" or "Swiggy" or "UPI credit" from the platform. Loan executives scan statements fast; they don't read every line. Highlighting your income for them can shave a day off processing. Small thing, works.

If you're an e-rickshaw driver

A specific profile with a couple of extra needs:

The base documents, plus a valid LMV driving licence, not just a learner's permit.

Six months bank statement if you have one. If your fares come partly through UPI, that history helps a lot.

Usually two references, ideally people who aren't your immediate family.

A guarantor for first-time drivers with no credit history.

⚠ The Aadhaar address trap (read this twice)

I'm pulling this out separately because it sinks more applications than anything else on the list.

If your Aadhaar shows your village or your parents' home, but you now live in a rented place in a different city for work, the lender sees a mismatch between your address proof and your Aadhaar. That mismatch alone gets applications rejected, even when everything else is perfect.

My friend from the start? His fourth rejection was exactly this. Old flat on the address proof, new flat on Aadhaar.

Fix it before you apply. Update your Aadhaar address at any UIDAI enrolment centre. Costs almost nothing, takes about ten days. Do this even if you're not buying anything right now, honestly, because future-you will need it for half a dozen things.

Documents at a glance — full checklist by profile

| Document | Salaried | Self-Employed | Gig Worker | E-Rickshaw |

|---|---|---|---|---|

| PAN | ✓ | ✓ | ✓ | ✓ |

| Aadhaar (current address) | ✓ | ✓ | ✓ | ✓ |

| Passport-size photo | ✓ | ✓ | ✓ | ✓ |

| Address proof (recent) | ✓ | ✓ | ✓ | ✓ |

| Salary slips (3 latest) | ✓ | — | — | — |

| Bank statement | 6 months | 12 months | 6 months | 6 months |

| ITR (2 years + computation) | — | ✓ | — | — |

| GST certificate | — | If registered | — | — |

| Business proof | — | ✓ | — | — |

| Platform partner ID | — | — | ✓ | — |

| LMV driving licence | — | — | — | ✓ |

| Guarantor / references | If asked | — | If new on platform | First-timers |

Why files get sent back — and how to avoid it

| Why your file gets sent back | What lenders see | Quick fix |

|---|---|---|

| Aadhaar address ≠ current home | Identity mismatch | Update Aadhaar (about 10 days) |

| 3-month bank statement (not 6) | Insufficient income pattern | Always bring 6 |

| Stale address proof | Doesn't reflect current residence | Use latest utility bill |

| ITR for 1 year only | Can't trend income | Bring 2 years + computation |

| No platform partner ID (gig) | Income source unverifiable | Screenshot from app, attach |

| Damaged CIBIL | Higher default risk | Add a guarantor, or improve score first |

A quick note on what comes after the documents

Once your documents are clean and submitted, the rest moves fast. For most profiles, an NBFC takes three to seven working days to decide and disburse. Banks take a bit longer, seven to fourteen. Rates across the board sit in a 12 to 19 percent band depending on your profile and credit. The paperwork is genuinely the slow part, which is exactly why getting it right in one go matters so much. If you're still finalising your savings versus borrowing split, our EV down payment guide walks through the maths.

Back to my friend

Fourth visit, he finally walked in with everything. Updated Aadhaar, six-month statement, salary slips, photo, address proof matching the Aadhaar. The executive went through it once, nodded, and that was that. Approved in a few days.

He laughed about it afterwards. "Char chakkar lagaye maine, jo ek list se bach jaate." Four trips that one checklist would have saved. That's the whole reason I wrote this down.

Print the list for your profile. Tick each item off before you leave home. One visit instead of four.

Where Credifin fits

We finance EVs across India through an online application, which honestly removes half the trip-to-the-showroom problem to begin with. You upload the documents once, from home.

What helps specifically: for gig riders and self-employed folks, we read the bank statement and platform payouts directly, so you're not stuck trying to produce salary slips you don't have. And our team flags missing documents upfront, in one go, rather than one at a time across four visits. Rates land 13 to 19 percent depending on profile, decision in 3 to 7 working days once your documents are in. The wider rate picture is in our EV loan India guide.

Bottom line

The documents are the slow part of any EV loan, and almost every delay is avoidable. Everyone needs PAN, Aadhaar (address matching where you live), a photo, and recent address proof. Salaried add salary slips and a six-month statement. Self-employed add two years of ITR, a 12-month business statement, and business proof. Gig workers bring the platform ID and the payout account statement.

Sort the Aadhaar address mismatch before anything else. It's the silent application-killer. Get your profile's list ready in advance and the whole thing takes one visit, not four.

FAQs

What documents do I need for an EV loan?

Base for everyone: PAN, Aadhaar (address matching current home), photo, recent address proof. Then salary slips and a six-month statement if salaried, or ITR plus business statement if self-employed.

Why do lenders want six months of bank statements, not three?

Six months shows a fuller pattern, income consistency, and how you handle money over time. Bringing only three is the most common reason salaried applicants get sent back.

Can gig workers apply without salary slips?

Yes. The platform partner ID and the bank statement showing payouts act as income proof. NBFCs read this; most banks can't.

What if my Aadhaar address doesn't match where I live?

Update it before applying. The mismatch gets applications rejected on its own. The update is cheap and takes about ten days.

Do I need a guarantor?

Often only first-time borrowers, gig workers new to a platform, or low-CIBIL applicants. Clean salaried and established self-employed usually don't.

How long does approval take once documents are in?

NBFCs 3 to 7 working days, banks 7 to 14. Clean documents are what keep it at the fast end.

Is income proof mandatory for an e-rickshaw loan?

Some form of it, yes, but a bank statement showing UPI fares plus references and a guarantor can stand in if you don't have formal documents.

What rate should I expect today?

12 to 19 percent depending on profile and credit score.

Ready to apply?

Want your EV loan done in one go, not four trips? Apply with Credifin online, upload your documents from home, and we'll flag anything missing upfront instead of one at a time. Decision in 3 to 7 days, pan-India.

Apply for an EV LoanThis might catch your interest