E-Rickshaw Loan Rejected? 6 Reasons and the Fix for Each

Lakshay Khanna·12 June 2026

Ramesh drives an e-rickshaw near the railway station in his town. Rented one for two years, 280 a day to a fleet owner, watching that money disappear into somebody else's pocket. Last year he'd had enough. Decided to buy his own.

Rejected. Twice.

Came to me looking properly defeated, convinced the banks had quietly decided he was "not the type they lend to." His words. Like there was a stamp on him somewhere.

Took me about ten minutes looking at his paperwork to find it. Both times he'd applied with zero banking history. All his fare money was cash, nothing in any account, so the lender had literally nothing to look at. He wasn't un-loanable. He was invisible.

"Mujhe laga meri aukaat nahi hai loan ki. Asal mein bas account hi nahi tha."

And that's the thing. E-rickshaw rejections almost always come down to a few boring, fixable reasons. Not a judgment on you. Here are the six, and what to actually do about each.

Rejected by a bank? An NBFC can usually still approve you.

Credifin reads your bank statement and fare pattern as income proof — no salary slip needed. Decision in 3-7 working days, application online.

Apply for E-Rickshaw Loan →The 6 reasons at a glance

| # | Why your file got rejected | The fix | Time to fix |

|---|---|---|---|

| 1 | No banking history at all | Open account, deposit cash fares, push UPI | 4-6 months |

| 2 | No formal income proof | Apply at an NBFC, not a bank | Immediate |

| 3 | No guarantor lined up | Relative with steady income + decent CIBIL | 1-2 weeks |

| 4 | Aadhaar address ≠ current city | Update at UIDAI centre | ~10 days |

| 5 | Forgotten small default | Pull credit report, clear it | 3 months |

| 6 | Applying everywhere at once | Pick one lender, fix the cause, wait | 60-90 days |

No banking history at all

Ramesh's exact problem, and easily the most common. Cash fares, nothing flowing through an account, so when the lender looks you up there's no trail. No trail, no visible income. No visible income, no loan. Simple as that, and brutal.

✓ FIX: Open an account. Even a basic one at a small regional bank. Then start pushing money through it, deposit your daily collection, and get passengers paying by UPI wherever you can so the income lands digitally on its own. Run it four to six months before you apply. Now there's something for the lender to read. That one move is what eventually got Ramesh his approval.

No formal income proof

Related, but its own thing. Even with an account, drivers rarely have a salary slip or ITR, nothing a bank's software recognises as "income."

✓ FIX: So stop walking into banks. Go to an NBFC. Honestly this is the single biggest lever in the whole list. NBFCs are built for exactly this, they read your bank statement and your fare deposit pattern and approve on that. A bank wants a document its system can tick. An NBFC reads the actual money moving. For a driver, that difference is everything — the same logic that helps delivery riders and other no-slip profiles get through.

No guarantor when one's needed

First-time driver, no credit history? Lenders often want a guarantor. Someone who effectively co-signs and reassures them. Don't have one lined up, and a thin application just stalls.

✓ FIX: Sort this before you apply, not during. A relative or friend with steady income and a decent CIBIL is enough. Doesn't need to be a rich person. Just a stable, willing one. A guarantor in hand often flips a borderline no into a yes, and sometimes shaves your rate down a bit too.

Aadhaar address doesn't match where you live

This one hits migrant drivers hard. Aadhaar still shows the home village in Bihar or UP, you're driving in a city three states away, the address proof and Aadhaar don't line up, and the whole thing gets rejected on that mismatch alone. Doesn't matter how good everything else is.

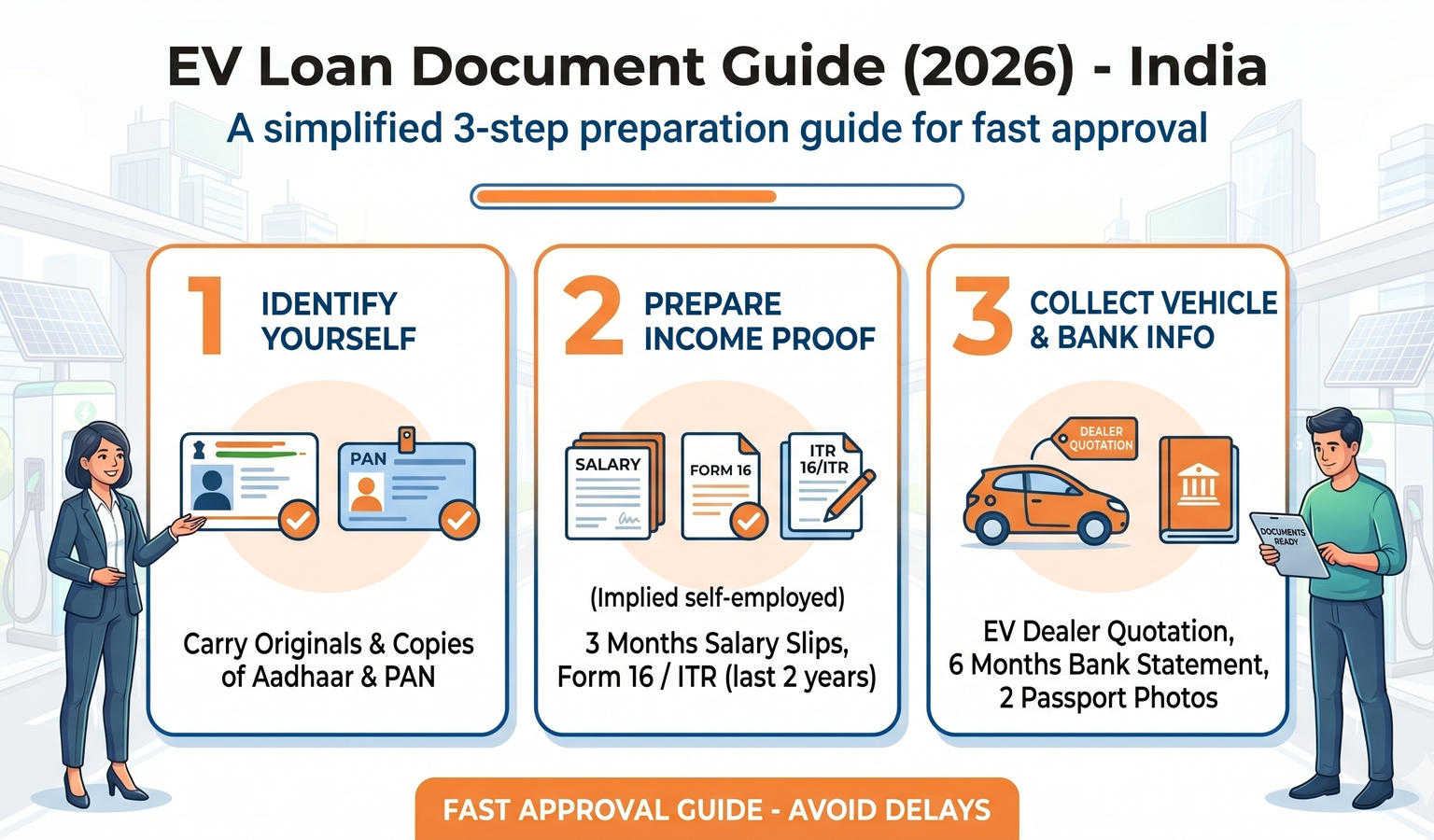

✓ FIX: Cheapest fix on this list. Update the Aadhaar address to where you actually live now, any UIDAI enrolment centre, about ten days. If you've moved for work, do this even before you're thinking about a loan. It blocks a lot more than credit. Full document trap details in our EV loan documents checklist.

A small unpaid default nobody remembers

Catches people completely off guard. A forgotten 4,000 on some app. A phone EMI you were sure had closed. A tiny overdue amount you'd genuinely forgotten existed. Any of it flags your file and triggers a rejection.

✓ FIX: Pull your credit report, it's free once a year through the RBI-mandated bureaus, and hunt for the thing. Clear whatever's sitting there. Then wait about three months for it to update. Most of the time the amount is small and the driver had no idea it was quietly sinking every application.

Applying everywhere at once

The panic move. You get a no, so you run to the next lender, then the next. Except every application is a hard credit pull, they pile up, your score drops, and the rejections multiply. You've turned one no into five, all by yourself.

✓ FIX: Pick one NBFC, maybe one bank. Apply there, full stop. Wait for the answer. If it's no, don't spray more applications, find the real reason from this list, fix it, wait 60 to 90 days, then try once more. Patience is genuinely cheaper than another five inquiries. Our bank vs NBFC decision guide shows how to pick the right one first time.

What an e-rickshaw loan should actually cost

Quick reality check so you know what you're aiming at. E-rickshaw loans currently sit around 14.5 to 18 percent, the top end of the broader 12 to 19 percent vehicle loan range, because the profile carries more risk on paper. Borrow 1.2 to 1.8 lakh over 24 to 30 months and your EMI lands somewhere around 5,000 to 7,000 a month. For a working driver that's a few fares. Set against the daily rent most pay a fleet owner, owning usually wins well within the loan term. And then the rickshaw's just yours. Wondering how much it'll actually bring in? Our e-rickshaw income & ROI guide runs the real monthly numbers.

| Loan amount | Tenure | Rate | Monthly EMI | Daily equivalent |

|---|---|---|---|---|

| Rs 1.2 lakh | 24 months | 15% | ~Rs 5,820 | ~Rs 195 |

| Rs 1.5 lakh | 30 months | 16% | ~Rs 6,080 | ~Rs 205 |

| Rs 1.8 lakh | 30 months | 17% | ~Rs 7,400 | ~Rs 250 |

Back to Ramesh

Nothing clever, in the end. Opened an account at a regional bank, deposited his daily cash, nudged passengers toward UPI. Five months later his statement showed a clean, steady fare income. Then he skipped the banks completely and applied through an NBFC with his brother-in-law as guarantor.

Approved. 1.45 lakh, 30 months, EMI around 5,800. Went from 280 a day renting someone else's rickshaw to roughly 195 a day owning his own.

He called me after, properly pleased with himself. "Pehle doosre ki gaadi chala raha tha, ab apni banegi." Same daily grind. Completely different ending.

Which is the whole point really. A rejection is almost never a verdict on you. It's a missing account, a mismatched Aadhaar, an absent guarantor, a forgotten bill. Every one of them fixable.

Where Credifin fits

This is exactly the borrower we're built for. We finance e-rickshaws for drivers and small fleet operators, and the whole assessment runs on informal income, not the documents a bank's software insists on.

We read your bank statement and fare pattern instead of asking for a salary slip you'll never have. We work with guarantors for first-timers. And if some small credit error is dragging your file down, we can usually see past it to the real picture. Rates for e-rickshaw profiles generally land in the 14.5 to 18 percent range, decision in 3 to 7 working days, application online so there's no four-trips-to-a-showroom nonsense. The wider rate picture across profiles is in our EV loan India guide.

Bottom line

E-rickshaw rejections come from a short, fixable list. No banking history. No formal income proof. No guarantor. An Aadhaar mismatch. A small unpaid default. Too many applications at once. Not one of them is permanent. (Buying an electric scooter or EV car instead of an e-rickshaw? The reasons differ slightly — see our EV loan rejected guide.)

Open an account and build six months of statement. Go NBFC, not bank. Line up a guarantor. Fix the Aadhaar address. Clear small dues. Don't shotgun applications. Do that, and the loan that felt impossible turns into a three-to-seven-day yes.

FAQs

Why was my e-rickshaw loan rejected even though I earn enough?

The lender probably couldn't see your income. Cash fares with no account leave nothing to assess. Build banking history first.

Can I get an e-rickshaw loan with no income proof?

Yes, through an NBFC. They read your bank statement and fare deposits instead of demanding a salary slip or ITR.

Do I need a guarantor?

Often, if you're a first-time driver with no credit history. A relative with steady income and a decent score works fine.

How do I build banking history on cash income?

Open a basic account, deposit your daily fares, push passengers toward UPI. Six months of that gives a lender something to read.

Already rejected twice, now what?

Stop applying. Find the real reason above, fix it, wait 60 to 90 days for your score to recover, then apply once through the right lender.

What's the EMI on an e-rickshaw loan?

On 1.2 to 1.8 lakh over 24 to 30 months, roughly 5,000 to 7,000 a month. Usually less than the rent paid to a fleet owner over the same stretch.

What rate applies today?

Generally 14.5 to 18 percent, the top end of the 12 to 19 percent vehicle loan band, because of the risk profile.

Will an Aadhaar mismatch really cause rejection?

Yes, on its own. Update it to your current city first. Cheap, about ten days, and it matters most for migrant drivers.

Ready to apply?

Turned down for an e-rickshaw loan? Apply with Credifin online. We assess on your real fare income and bank statement, work with guarantors for first-time drivers, and tell you straight what to fix. Decision in 3 to 7 days, pan-India.

Apply for E-Rickshaw LoanThis might catch your interest